HSC corporate treasury seeks to acquire Treasury Services from a bank by fulfilling several key qualifications that reflect the bank’s need to manage credit risk, operational risk, and regulatory compliance

Source of Fund and Wealth

- Personal Funds – Pain-in Capital

- Collateral – Investment Proceeds

- Securitization – Contract Obligations

- General Ledger – Treasury Ledger Reserves

Capital Ownership

Funds are wholly owned by HSC and are:

- not representing non-affiliate deposits

- not pooled third-party funds

- not received for money transmission

- not escrowed for public benefit

- not subject to repayment on demand

Regulatory Representation

HSC does not operate as:

- A Money Services Business

- A payment intermediary for the public

- A payment activity unless through a bank payment rails under UCC Articles 3, 4, and 4A, for final settlement.

Controls & Oversight

The following certification is provided to support bank’s treasury service enablement and satisfies internal review standards consistent with FFIEC and FinCEN guidance.

- Full AML/KYC, CDD, and OFAC screening performed on all counterparties

- Audit-ready internal ledger with immutable transaction records

- Dual authorization on treasury disbursements

- Quarterly internal audits and annual external review

Treasury Technology

HSC operates a closed-loop treasury architecture designed to ensure payment finality, regulatory clarity, and audit integrity while leveraging bank-recognized payment rails.

Payment

HSC utilizes the following legally recognized wholesale payment mechanisms:

- UCC Article 3 – Negotiable instruments and digital equivalents for settlement and traceability

- UCC Article 4 – Internal deposits, collections, and book transfers within the depository institutions and

- UCC Article 4A – External wire and funds transfers with irrevocable settlement.

Transactions

Distributing EFT between HSC treasury ledger and bank accounts Subject to AML/KYC, source-of-funds validation, and FFIEC BSA/AML review Finality achieved via book entry or internal sweep Executed via UCC 4A wires Bank provides settlement confirmation and legal finality Reconciled GL-to-GL

Ownership & Control

HSC remains principal owner of funds at all times No custodial holding for the public No intermediary transmission risk

Ledger Architecture

Single source of truth treasury ledger Transaction-level attribution (origin, purpose, counterparty) Immutable audit logs

Controls

Dual authorization for all disbursements Automated sweep rules with thresholds Daily reconciliation against bank statements Except reporting and escalation protocols

Audit Readiness

Quarterly internal audits Annual independent review Retention of records consistent with BSA/AML and SEC requirements

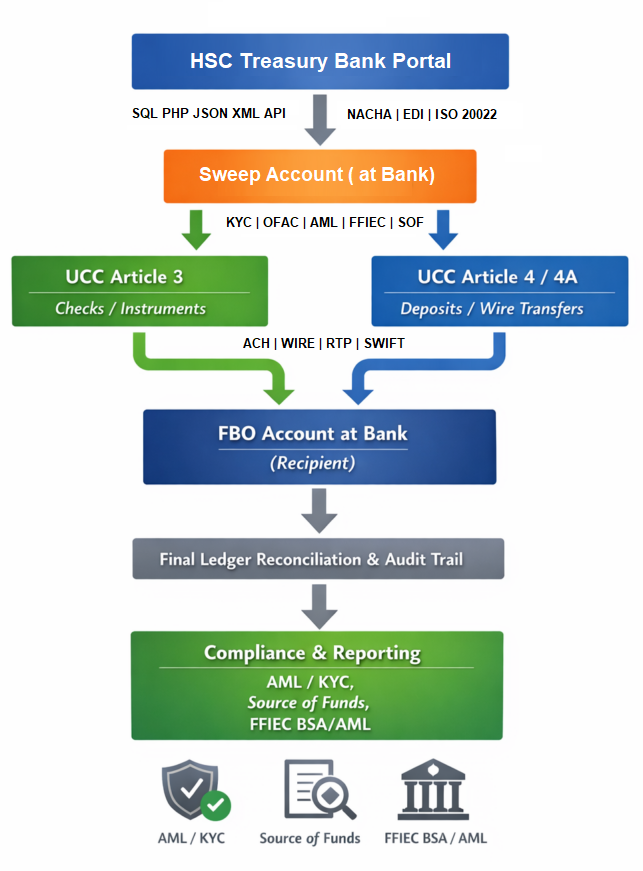

Flow of Funds Diagram

Transaction Flow – Example

Step 1: Internal Treasury Ledger → Credit Transfer to Clearing account

- HSC posts entry in internal ledger.

- Generates UCC-compliant notice of transfer.

Step 2: Clearing Account → FBO Bank Account

- ACH or Wire transfer executed.

- Bank confirms receipt under UCC 4/4A.

Step 3: Beneficiary Account Access

- Funds are available to final beneficiary.

- Audit trail ensures compliance and finality.

Initial Deposit $250 – $750k

(30 – 90 Days

- “The initial deposit is intended to establish baseline treasury liquidity for HSC’s operating and investment activities.

- The balance is sized to support wire and ACH credit activity, treasury sweeps, and liquidity positioning, while allowing conservative transaction limits during the initial monitoring period.

- Funds represent corporate capital contributions and related-party transfers only. The account will not be used as a pass-through, custodial, and third-party payment account.

Deposits will be used for:

- $200,000 – Home office facilities

- $150,000 – Equipment and technology upgrades

- $100,000 – Marketing and sales expansion

- $50,000 – Hiring key personnel

Days 0–30: Establish & Observe

Balances

- Initial funding: $250k–$300K

- Minimal volatility

Activity

- 2–4 inbound related-party transfers

- 2–5 outbound wires (investment / operating)

- No ACH debits

- No third-party collections

Bank Benefit

- Clean baseline transaction profile

- Limits typically set conservatively

Days 31–60: Controlled Usage

Balances: Stable or modest increase (+$450k–$700k)

Activity

- Regular wires (investment allocations)

- ACH credits (vendors / entities)

- Treasury sweeps activated

- Monthly reconciliation delivered if requested

Bank Response

- Limits reviewed

- Reduced manual review

- RM escalates relationship internally

Days 61–90: Treasury Normalization

Balances: $1.25M–$2.5M typical

Activity

- Predictable cadence

- Higher wire limits

- Same-day ACH (if requested)

- Investment settlement flows

Bank Outcome

- Treasury Services considered “seasoned”

- Faster approvals

- Expanded service eligibility

3 Year deposit projections

- Year 1: $750,000

- Year 2: $1.2 Million

- Year 3: $2.0 Million

Risk Assessment

Treasury activity consists of prefunded, corporate treasury-initiated payment orders settled via established wholesale payment systems with immediate legal finality.

Activity presents low settlement, credit, and compliance risk:

Uses final settlement rails Avoids provisional credit Maintains clear ownership and purpose

Bank’s Benefit

Eliminates Credit & Settlement Risk

Funds enter the bank already settled No provisional credit No float exposure No return windows

Clean Source-of-Funds

Funds originate from known corporate capital Beneficial owners are documented No public or retail customer funds Push-only payment activity

Reduced Regulatory Classification Risk

No money transmitter or payment processors internal treasury accounting identified beneficiaries Avoids consumer funds and payment services

Stable, High-Quality Deposits

Large, predictable balances Low transaction volatility Long holding periods Non-rate-sensitive capital

Fee-Based Revenue (Low Cost to Serve)

Wire fees, Treasury service fees, Account maintenance fees FX / custody (if applicable)

Operational Simplicity

Fewer reversals Cleaner reconciliations Clear authorization chains Lower fraud exposure

Examiner-Safe Client Profile

Prefunded wires Transparent ledger logic No consumer exposure Clear economic purpose

Long-Term Strategic Relationship Value

Multi-product lifetime value Relationship moat Low churn

“HSC delivers stable, prefunded treasury balances with low settlement, credit, and compliance risk while generating fee-based revenue at minimal operational cost.

Bottom Line

This method benefits the bank because it:

✔ Reduces risk

✔ Simplifies compliance

✔ Produces stable deposits

✔ Generates predictable fees

✔ Avoids regulatory classification problems