Intra liquidity

Community treasury and banking for subsidiary investments

1. OVERVIEW

HSC offer Treasury Banking Portal for subsidiaries, contractors and vendors that are account holders with HSC’s banking partner.

2. What is the Treasury Bank Portal

A ‘Treasury to Bank Application’ T2B used for community investment underwriting for subsidiaries members. Also provides ‘Primary Credit Facility and Liquidity’ for Community Investment Programs (CIPs).

- Treasury Accounts for Internal custody, credit facility and investment liquidity as follows:

- Partnership

- Administration

- Development

- Investment

- Banking

- Audit Trails

- Bank Accounts:

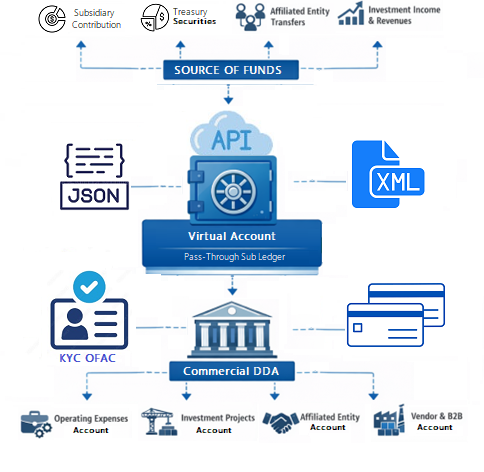

- Virtual Account Sub Ledger – serves as a “conduit” to pass funds from Treasury Bank Portal through a specific Virtual Account Number (VAN) assigned to the subsidiary or vendor DDA.

- Operating Fiduciary DDA – for fiduciary compensation

- FBO Project DDA – for capital projects expense as segregated funding.

3. TREASURY SOLUTIONS

Designed to maintain strong financial controls and clear audit transparency with the following:

a. Membership-

Creating private public partnership between HSC, subsidiaries and depository banks accountholder.

b. Administration-

- Delegation of Authority

- Meeting and Board Resolution

- Service Level Agreement

- Work Orders & Invoicing

c. Development –

- Planning & Programming

- Internal & Third-Party Appraisal

- Debt-Service Coverage Ratio (DSCR) as needed

- Legal Counsel

- Financial Review

d. Investment –

- Asset Certification

- Equity Assessment

- Margin (Inhouse Credit Facility)

- Bond Creation & Assignment

- Novation Netting Assignment

e. Banking

- Virtual Bank Account

- DDA Bank Accounts

- KYC, AML, OFAC

- Credit Facility (as needed)

- Payment (ROI, Compensation, or expenses)

f. Audit

- Transparency for Bank Examiner and Business Relationship Manager.

- Ledger Reconciliation

- Data Archive

- Third Party Auditoror fiduciary compensation

4. Banking Services

Integrated “Book Transfers” as a “Payment Factory”

- Payment Rails External rails like ACH or Wire.

- Book Transfers (internal transfers between accounts at the same institution) to achieve instant settlement and zero transaction fees.

- Automated Sweep Automate internal virtual account pass-through, Instead of manual entry,

- Unified Visibility: Link all subsidiary accounts under one master login to maintain your “source of truth” for liquidity.

- Commercial Cards: For subsidiary officers and SPV

- Role-Based Access: Assign specific permissions for each subsidiary while maintaining centralized control level.

- Batch Processing: Upload a single “payable file” containing multiple internal transfers. The system automatically identifies the recipients as existing Capital One accounts and processes them as Book Transfers.

- Intercompany Tracking: This ensures the central treasury remains the “source of truth” while allowing subsidiaries to operate with their own sub-accounts.

- Direct Connectivity: Allows HSC Treasury Bank Portal to trigger internal book transfers directly from your software without logging into the portal, streamlining the “liquidity liquidation” process for alternative investments. via H2H JSON API Integration XML ISO 20022

5. Risk Mitigation for the Bank

The bank does not provide Credit or Liquidity, which significantly reduces the bank’s exposure as following:

- Reduced Credit Risk: No bank credit facility or extending a line of credit.

- Off-Balance Sheet (Sub account) Treatment: The bank does not hold the legal obligation for credit transfer through the sub ledger activities, because it remain off the bank’s balance sheet and only appear on your internal Treasury Bank Portal ledger until finalized.

- Technology Layer: The bank’s Treasury strictly providing payment factory for HSC’s own capital movement.

- Elimination of Intraday Exposure: By using pre-funded virtual accounts rather than zero-balance accounts (ZBAs) that rely on bank-funded “daylight” overdrafts, you remove the risk of unsecured intraday lending as credit facility for the bank.

- Operational Risk Focus: HSC utilize the bank’s API calls for automation vs manual transactions

- KYC/OFAC/AML with subsidiary bank accounts with transparent contracts and “Source of Truth” maintained.

6. Intra Liquidity for Private Funding:

A. Intercompany Netting:

Settle debts between subsidiaries internally. This “private” settlement reduces transaction fees and the volume of funds moving through external banking rails.

B. Capital Management:

- Capital contributions and investment funding

- Expense disbursement and vendor payments

- Cash concentration and liquidity management

- Internal accounting and reconciliation

- Financial reporting and audit support

C. Private Funding Sources:

- No public customers

- No retail deposits accepted

- No third-party payment services

- No money transmission activities

- No commingling of unrelated funds

“All funds represent corporate capital contributions, affiliated entity transfers, or project-related payments.”

7. BENEFICIARIES & STRUCTURE

All Beneficiaries are Trust Deposit Accountholders that’s grandfathered in under corporate trust membership. It is managed by the Hill Scott Corporation (HSC), a S Corp that’s 100% owned and lead by its founder Hillery M Scott, CFO, as Chief Fiduciary Officer.

• Revenue collection and capital funding

• Operating expense disbursement

• Intercompany cash concentration

• Investment project payments

• Vendor and payroll processing

“The banking relationship will serve as the primary settlement platform for all external financial transactions.”

8. SOURCE OF FUNDS

Funds are private funds from subsidiary members within the corporate treasury ledger with 1:1 ratio to nations fiat currency.

Types of Funds are:

- Cash and cash equivalents

- Corporate capital contributions

- Affiliated entity transfers

- Investment securities

- Contractual project revenues

- Credit Notes with Invoices

- Vendor payments and operating expenses

- Intercompany asset transfers between affiliated entities

- Custody Agents, and bank financial statements

“No consumer funds or public deposits are accepted.”

9. TRANSACTION

Typical characteristics:

- Moderate transaction volume

- Stable account balances

- Low transaction volatility

- Push-only payment activity

10. INTERNAL CONTROLS & GOVERNANCE

HSC maintains a comprehensive internal control framework with delegation of authority to ensure transparency and risk management.

Key controls include:

- Board Meeting and Resolution

- Dual authorization for disbursements

- Segregation of duties for treasury functions

- Daily reconciliation with bank records

- Formal approval thresholds for payments

- Documented audit trails for all transactions

All counterparties are subject to standard due diligence procedures.

- Entity Verification: Banks perform Know Your Customer (KYC) and Know Your Business (KYB) checks at the legal entity and physical account level. This includes identifying beneficial owners with a 25% or greater stake.

- Transaction Monitoring: Bank partners must monitor transaction patterns for suspicious activity to comply with the Bank Secrecy Act (BSA) and the USA PATRIOT Act.

- Reporting: Banks file certain high-value transactions, Currency Transaction Reports (CTRs) will be filed with FinCEN within 15 days

- Arm’s Length Principle: Intercompany transfers must comply with “arm’s length” pricing. If tax authorities determine transfer prices are not market-rate, they may adjust taxable income and impose penalties.

- Cash Segregation: HSC has specific cash segregation mandates, and ensure each virtual account structure mirrors these requirements legally.

- Segregation of Duties: Enforce workflows requiring with auditable evidence and multiple approvals for fund movements.

- GLBA Compliance: The Gramm-Leach-Bliley Act (GLBA) mandates that financial organizations implement technical safeguards to protect customer

11. ACCOUNTING & AUDIT PRACTICES

HSC maintains internal accounting systems to support financial reporting and reconciliation.

Practices include:

- Detailed transaction attribution

- Routine internal audits

- Independent annual review

- Record retention consistent with financial regulatory standards

12. RISK PROFILE

HSC activity presents a low operational risk profile due to:

- Prefunded payment structure

- Clear ownership of funds

- No third-party custody services

- Limited transaction types

- Full transparency of economic purpose

All payments are settled through regulated bank-operated payment systems.

11. INITIAL DEPOSIT PROFILE

First quarter is expected to range between: $250,000 – $750,000

Projected deposit growth is anticipated based on investment activity and capital deployment cycles. Funds represent long-term corporate capital rather than short-term transactional balances.

12. EXPECTED ACCOUNT BALANCES

| Category | Estimated Range |

| Initial Deposit | $250,000 – $750,000 |

| Average Monthly Balance | $1,500,000 – $4,000,000 |

| Peak Balance Range | Up to $8,000,000 |

| Balance Volatility | Low to Moderate |

| Primary Funding Type | Corporate capital |

Balances are expected to be stable and non-seasonal.

13. EXPECTED TRANSACTION VOLUME

ACH ACTIVITY

| Type | Monthly Volume |

| ACH Credits (Outbound) | 20 – 60 |

| ACH Debits (Inbound) | 10 – 30 |

| Typical Amount Range | $1,000 – $25,000 |

Purpose:

• Vendor payments

• Operating expenses

• Routine project costs

WIRE TRANSFERS

| Type | Monthly Volume |

| Domestic Wires Outbound | 5 – 15 |

| Domestic Wires Inbound | 2 – 8 |

| Typical Amount Range | $50,000 – $500,000 |

| Largest Expected Wire | Up to $1,500,000 |

Purpose:

• Capital deployment

• Investment funding

• Real estate and equipment purchases

1. CAPITAL SOURCES (Inbound Funds)

- All incoming funds originate from known related parties or contractual business activities.

- No public deposits or retail funds are accepted.

2. CENTRAL TREASURY ADMINISTRATION

Internal:

- Cash concentration

- Transaction authorization

- Internal accounting reconciliation

- Payment approval controls

- Audit documentation

External:

- Subsidiary Funds

- Family Office Corporate Treasury

- Investment SPV Trust

- Receivables / Bonds / Investments

- Bank Virtual Account / POBO – COBO

- Subsidiary Fiduciary DDA

14. Virtual Account Breakdown

virtual accounts act as pass-through vessels that collect incoming payments and immediately route them to a linked primary HSC (master) bank account. While the VA does not hold an end-of-day balance or settle funds, it is designed specifically to receive and “pass over” money for organizational and tracking purposes.

How they collect and pass money

- Unique Identifiers: Each virtual account is assigned and linked to a subsidiary treasury account that linked to a unique account number at the bank (like a virtual IBAN).

- Settlement: When a payment is sent to a virtual account, the funds pass thought the virtual layer and settle directly into the linked physical master account.

- Mirroring: The virtual account “mirrors” the transaction, creating a digital record (sub-ledger) that shows a credit for that specific account, even though the actual cash is in the primary account.

- Automatic Routing: This structure allows a business to assign different virtual accounts to different customers or departments. When money arrives, the system automatically knows exactly who it came from based on which virtual number was used.

Comparison: Virtual vs. Physical Accounts

| Feature | Virtual Account | Physical Account |

| Holds Balance | No (sub-ledger only) | Yes (holds actual funds) |

| Settles Funds | No (settles on primary) | Yes |

| Unique ID | Yes (Virtual IBAN/Account #) | Yes |

| Speed of Setup |

15. ISO20022 DATE MAPPING

TBP utilized ISO 20022 JSON API Data Mapping (pain.001) for key is the distinction between the Debtor (Treasury Bank) and the Ultimate Debtor(The Subsidiary).

Standard Specific Requirements

- Structured Addresses: Separate tags for Street, Town, Country) rather than a single string to comply with global AML regulations

- Purpose Codes: <Purp> tag with a 4-character code to avoid regulatory delays.

- Instruction Identification: Ensure the <InstrId> is unique to prevent duplicate payment processing within the gateway.

Integrative Implementation

Treasury has three standard integrative paths: Custom API, Middleware (iPaaS), or Host-to-Host (H2H):

- Custom API Development: TBP is a PHP/MySQL application that supports extensions and custom modules. It can build a custom module that calls the bank’s Payments Developer Portal APIs.

- Middleware (iPaaS): TBP or HSC can use a third-party integrator which has a direct bank integration, to act as a bridge. TBP would connect to the middleware, which then handles the complex bank communication.

- Host-to-Host (H2H): The bank can provide a secure SFTP for file transfer. TBP would generate the ISO 20022 XMLfiles (as discussed previously) and drop them into a secure folder for the bank treasury to pick up and process.

Security & Authentication:

TBP provides mutual TLS (mTLS) or OAuth with CA-signed certificates.

TBP is web-based, and its server will be configured to handle these secure handshakes.

- Automated Actions: TBP utilize “Automate Actions” feature to trigger a subsidiary bank payment when a record status changes (e.g., when an invoice is “Approved”).

- Webhooks: To achieve real-time reconciliation (COBO) to TBP module to update payment statuses automatically within Treasury Bank Portal’s database.